Several years ago, when Equity.Guru boss Chris Parry was writing at Stockhouse, he was called out to a new client – a company called Abattis Bioceutical (ATT.C).

Abattis execs had just signed a marketing deal with Stockhouse to help tell their story to investors, and were excited for what might follow.

As Parry tells it, he walked into the boardroom and sat down, and told the collective execs what was going to come next.

“You’ve got eight verticals in this thing and nobody knows what they are, what’s real and what isn’t, and how they might work together, so I’m going to write eight stories – one on each vertical – and dig right into them all. We’ll tell the world exactly what you have so you can move forward with a clear story,” he said.

The execs didn’t embrace this strategy.

“Maybe we could just keep it general,” said one, adding, “We don’t want to overwhelm investors.”

But Parry was insistent. “This is a new sector and there’s a lot of bullshit out there, a lot of fake assets. Let’s set you above it all, show ’em what you’ve built.”

The next day, then CEO ‘Maserati’ Mike Withrow called Stockhouse and backed out of the signed contract.

“We don’t think we can leash Parry,” was supposedly the reason given.

But there was another reason, a rather important one that soon became obvious; Abattis didn’t have shit. It was a pile of cardboard cutouts of real companies, with nothing behind them but an incorporation document and a logo. That played great at investor conferences but the moment folks tried to look under the ATT skirt, they’d find actual junk where ‘the junk’ should have been.

For years, Parry says, whenever he would be at a conference or cannabis event, someone would inevitably ask whether Abattis was cheap enough to buy into yet.

“No,” he’d say. “It’s not at zero yet.”

Now, it kind of is.

CSE bulletin 2019-0808

The common shares of Abattis Bioceuticals Corp. will be delisted at the market close on Aug. 9, 2019. Abattis Bioceuticals is currently suspended. See bulletin 2019-0206.

The most recent Abattis news releases still contain the line, “Abattis is positioned to be a leader in the cannabis industry as a fully integrated medicinal cannabis company.” None of those words are true in the sequence in which they’ve been placed.

Abattis is all but gone, to be delisted from the CSE, where you can literally get a sweatshop of nuns skinning puppies to be sold as cashmere listed. By God, we’ve seen some terrible things on the CSE over the last few years, but it turns out Abattis is too shitty even for the Cannabis Stock Exchange.

The time has come for the lords of the flies to ‘kill em ’til they’re dead.’

But how did this company, once valued in the hundreds of millions of dollars, become so awful that three sets of auditors and the Crazy Eddie of stock exchanges couldn’t get through their paperwork in time enough to keep them listed?

It had a LOT of help on that front.

The African Spotted Hyena uses an attack-mode called Swarm Intelligence – to disorient and overwhelm its prey before ripping off chunks of its flesh. The Toronto Venture Exchange (TSX.V) and CSE are a Savannah crawling with their own pack of Spotted Hyenas.

Their name is Bridgemark Financial and their prey has been both CEOs who thought they were on their side, and the retail investor who didn’t see them coming.

According to Bridgemark’s website it can help “raise additional capital through private placements, initial public offerings, or reverse mergers.” On the website, there is no “Our Team” link – or any listed employees, likely for their own safety as much as any other reason.

Reported Bridgemark pack (members & associates) includes Simran Gill (CFA), Anthony Jackson (CPA), and Justin Liu (WTF).

The investor-rights group, #AllSharesMatter claim that there are 15 more members of the Bridgemark pack, though dozens more beyond that have been called to answer for themselves at regulatory committees looking for answers to serious questions. Wives and sisters and fathers-in-law have also been dragged.

@anon: Why are all of these companies using 1199 West Hastings Street Vancouver? Who is Anthony Jackson? Who founded Bridgemark? Why are social media and websites being scrubbed and erased?

@DogsFerDev: Plenty of snickers about Anthony Jackson and Bridgemark. Their roots in the Vancouver market run deep and the stories of people they’ve fucked over are endless.

@wdv: “We will get these clowns. Bridgemark fucked with the wrong company shareholders!”

@BrettCross: If Bridgemark is a company you are invested in, then you should do some DD on some of their other plays.

Commentators on Ceo.ca – claim that the “other plays” include: $ITG $CRYP $AFI $BCFN $DNAX $NINE $UAV $ZNK $KBEV $MDM $MY $SUV $VAX $KCC $LEO $LIC $NSAU $NTM $QBOT $WRW $PLAY $EASY and $ATT. That’s a big spider web, and the spider is still spinning it.

If we tried to dig into the whole nine yards, we’d be here ’til next year, so let’s dig into one of their victims/accomplices/clients, Abattis Bioceuticals (ATT.C) and see how the game worked.

Abattis is actually the perfect example of the Bridgemark scam in action, because it shows how executives are all too happy to jump at into the arms of a bigger villain than themselves, will risk everything for a quick shag in the markets restroom, and will claim until their dying breath that ‘y’all just don’t understand, ya dumb retail kooks.’

Bridgemark’s scam (come at me, lawyers) was to offer around $4 million in financing to companies in return for $4 million in shares of the company (mostly free trading), and $3 million back to Bridgemark in ‘marketing costs’, which it appears were seldom backed by actual work.

Most CEOs would see they were going to get burned by this, and would refuse. But enough were desperate enough for dough that they’d drop to their knees and work it like a 1970’s secretarial pool.

In the case of Abattis, their knees were as calloused as they were open for business.

In February last year, when blockchain was big for a hot minute, Abattis announced a big deal, paying as much as $7 million for 49% of a blockchain company, Cannanumus, which was going to do an ICO for a cannabis crypto coin that it wouldn’t be hard to see was bullshit.

The deal was well received by the market, as it was intended to be, running the market cap up to $200m plus. But that value was also quickly destroyed as mysterious selling quickly set in, ripping the stock back down in days.

Though it touched $200m, Abattis was actually only a $50m+ company for about two weeks. That’s how long it took for the Bridgemark stock to get ripped, and for retail investors chasing that rise to lose everything.

The details of the deal, which most investors still have never looked at because it’s SUCH HARD WORK TO READ, showed a transaction between buddies where shareholders were used as the tissue after Bridgemark had finished pulling a train on the company.

Let’s have TheDeepDive.ca take it for a turn.

So where’s the benefit to Abattis for this expensive acquisition? As of yet, this is yet to be seen. Arguably no value has yet been acquired by the organization. When we did a Deep Dive into the company though, we noticed some connections. Cannanumus itself was founded by Simran Gill, who from what we can tell, is a Principal at BridgeMark Financial. On the surface, this appears to be a non-issue.

However, BridgeMark Financial was founded in part by Anthony Jackson, the former CFO of Abattis Bioceuticals. Shortly after the acquisition of Cannanumus, Jackson resigned from the firm and was replaced with the current CFO David Whitney. Interestingly enough, Jackson also had a connection to the recent acquisition of Green Tree Therapeutics as well, wherein he was a shareholder of the company that formerly owned the rights to the firm. After Green Tree was acquired by this previous firm, that too is when Jackson made his exit.

It remains to be seen what exactly Abattis will be receiving in exchange for its seven million dollars. As it stands, it seems that the beneficiaries are former members of management rather than the current shareholders.

If this kind of action makes you grossed out that the markets aren’t better policed, you’re going to hate the four years prior, where Abattis pulled this on a minor league scale repeatedly and nobody raised a damn eyelid.

[contextly_sidebar id=”UBkNAPtJwj5RMqx4sxfU0WroZTgUlhEY”]Today, ATT claims to provide “integrated solutions for cannabis based and natural formulations, extracts and product development from concept to market delivery.”

That’s code for ‘cannabis vertical integrator.’

But a vertical integrator buys things that one can reasonably integrate; real companies with real assets that, when combined with other assets acquired from elsewhere, become worth more than the sum of their parts.

As an example, a licensed producer might like to have their own lab, which can do their testing cheap and as a priority, make a little side money from competitors, and become profitable just off the work their parent company brings them. Win/win.

But what happens when the lab doesn’t have any actual lab equipment? What happens when folks visit and finds a Truman Show-like set-up, where if you open the wrong door you find the closet where the lab coat costumes are kept and the clipboards that fake scientists hold as you roll the media guys through?

That was the situation at Medijean, a Richmond BC-based weed company without any licensing that was ‘building for the future’ several years back and rolling journos through a fake tour of a fake lab, even as Health Canada was rejecting their license application. Medijean had nothing to do with Abattis (that I know of), but was the first fake cannabis deal to get flipped out of existence, while others were still making hay.

Abattis’ early life was pockmarked with ‘amazing’ acquisitions, almost always for shares, that ended up being worthless but which cost ten times more than the ‘fair value’ consideration given to them. Like PPRB and Pacific Bio back in 2009, which were supposedly supplying valuable patents needed to get the company going, and which cost $5 million in shares on a $500k fair value in 2009 but were abandoned by 2013 for a loss.

Or the 2012 acquisition of the BioPharma patent license of Nick Brusatore’s Vertical Designs, purchased for $6 million in shares on a fair value of $500k, which were then fought over in court because, well, Nick had a tendency to do exclusive deals to multiple companies, patents be damned.

Or the license pending weed grow they’re supposedly building on BC’s Gabriola Island, which is only accessible by seaplane or ferry, and thus a TOTALLY FUCKING RIDICULOUS PLACE TO PUT A CORPORATE WEED GROW.

Abattis is currently completing the build out of a 26,000 square feet facility on Gabriola Island through its wholly owned subsidiary Gabriola, which is in the late stages of completing its application to become a Licensed Producer. It is expected that this will occur in late 2018.

It has not occurred by mid-2019 and, frankly, it won’t occur ever.

There hasn’t been an MD&A filed by Abattis since July 2018, mostly because no auditor has been able to make sense of their dealings, but this passage from the most recent MD&A stood out to me:

During the nine months ended June 30, 2018, the Company issued an aggregate of 52,854,896 common shares for an aggregate fair value of $16,325,648 for settlement of trade payables and as consideration for services to consultants, directors and employees of the Company.

More:

Management and consulting fees increased to $17,973,534 for the nine months ended June 30, 2018 from $2,795,925 for the same period in 2017. The increase was primarily a result of building the core team needed to support the business as it continues to grow both through acquisitions and organically, as well as payments made to stakeholders involved in key acquisitions during the period.

Sweet Jesus.

That MD&A also shows $7.8m in assets listed by the company, with $69m of shareholder equity spent to get them.

Loss of $6,940,704 in the three months ended June 30, 2018 was higher than the loss of $2,030,728 in the same period in 2017. This increase is mainly due to an increase in management and consulting fees incurred by the Company during the current period in connection with business acquisitions.

It’d make you scream if you were the one buying their stock while they were handing your cash out to themselves, wouldn’t it?

But it’s always been this way. Let’s head back to January 28, 2015:

The Company would like to clarify it’s disclosure in terms of the March 24, 2014 news release, which can be found on the Company’s website and on SEDAR. The Company never stated that we “own” any MMAR licenses. What the Company has stated/disclosed is that we “have access” to MMAR licenses (which we do through a number of contacts, both personal and professional) which can “potentially” be transferred to our facilities

And:

On June 9, 2014, the Company’s material change report stated that several of its subsidiaries were in the late stages of the MMPR licensing process. The Company wishes to retract this statement

The early exec team were also on the grift.

During the nine months ended June 30, 2014, 5,619,100 incentive stock options with an estimated fair value of $4,915,287 were granted by the Company to certain directors, officers and consultants of the Company to purchase up to an aggregate of 5,619,100 common shares of the Company.

Which ultimately gave rise, in late July of this year, to this:

[Outgoing auditor] DMCL indicated that it did not have sufficient or satisfactory audit evidence to complete the audit mandate and verify as bona fide and arm’s length certain of the Corporation’s transactions involving acquisitions, investments and payments made to consultants and the value received by the Corporation in connection with such transactions

That was, essentially, the end of Abattis, just as it has also been with Wayland Group (WAYL.C), which also hasn’t been able to explain it’s dealings to auditors and are now on their third set, and getting close to their own delisting if the timing of Abattis’ is any indication.

My grander point in all this is to highlight that this was not a group of people just too simple in the noggin to be dealing with other people’s money.

THEY STOLE FROM YOU.

They did it brazenly as you like, a little at first, a little more subsequently, and then a whole shit ton more until the regulators FINALLY dug in.

To be sure, the Venture markets are built around separating the weak money from the strong, and you all willingly play because you believe there are enough people out there dumber than you to get an edge for yourself.

That’s the pact we make; that if we get shafted, it’s on us and we’ll do better next time.

But when the rules aren’t followed, the game isn’t square.

I don’t blame Mike Withrow for filling his pockets back in the day, because a lot of players were doing just that and still delivering some value for it.

“$4m for me, $400m market cap for you..” – I can live with that.

But these fucking nimrods at Abattis were taking $16m from you, and delivering $16m in losses, a giant yoink on their market cap, handing out cheap paper by the metric ton to anyone who’d give them 10c on the dollar for it, and doing whatever they could to disguise it all to you guys, telling you they were building something amazing at the end of it all.

It wasn’t a ‘market play’, and it wasn’t high risk/high reward… it was a grift.

And the biggest grifter in the bunch was this guy right here below, a cat who shouldn’t be allowed back near a pubco going forward.

“As the market shifts its focus from cultivation to downstream products and services, Abattis is uniquely positioned to become an industry leader in providing these services,” stated Abattis CEO, Robert Abenante – a young, bright, smooth-talking CPA, in this video that announced him to the world.

I’m going to let Lukas Kane take it from here because I’m too indignant to continue.

TAG OUT – Chris Parry

TAG IN – Lukas Kane.

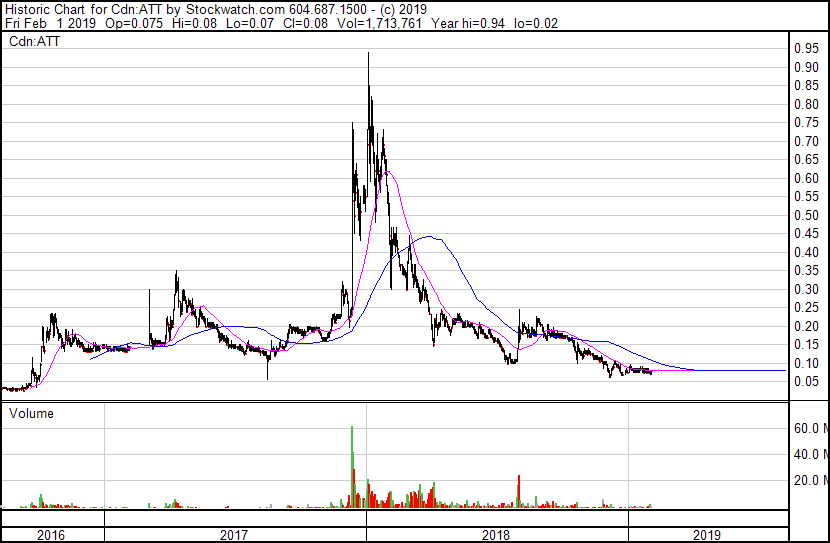

Since hitting a high of .83 on January 3, 2018 – Abattis fell to .10 on July 26, 2016 – then doubled to .20 on Sept 4, 2018 – then….kept dropping.

Let’s start our forensic examination of ATT on June 15, 2017 when Abattis appointed Anthony Jackson as CFO.

According to the press release, Anthony Jackson is a Chartered Accountant, who was “the founder and principle at Bridgemark Financial.” The ATT shareholders were assured that Jackson “will report directly to Robert Abenante, President and CEO of Abattis.”

Remember the “spider web” we mentioned early?

It has 3 dimensions.

One is time.

Over the years, Jackson has entered and exited CFO positions in a galaxy of publicly traded companies including, Greatbanks Resources, Katipult Technology, Dorex Minerals, Global UAV Technologies, Crystal Exploration, Sandfire Resources America, Coronet Metals, Oil Optimization, Montego Resources, Metropolitan Energy, Kaneh Bosm, Tiller Resources, Mediterranean Resources, Altan Rio Minerals, Eyecarrot Innovations etc.

[contextly_sidebar id=”UcdyhjOHWaOfi2QNYta37SQzEl4wQZ2s”]He was also appointed the CEO of Fire River Gold and Intact Gold Corp.

With a resume like that, Jackson can hardly be blamed for every nefarious subplot rising like a toxic vapour from investor bull-boards. But the presence of Bridgemark Financial coincided with an explosion of red flags.

Case in point: On November 30, 2017 Winston Resources (WRW.C) appointed Anthony Jackson as Director.

Jackson’s investment group purchased 6,410,518 common shares of Winston at .0156 representing 65% of the float, for a payment of $100,000.

Winston Resources had previously executed a reverse takeover of Green Tree Therapeutics – which owed a brand of vaporisers and some cannabis medical dispensaries.

To close that deal, Winston agreed to issue 10 million common shares to Green Tree shareholders at a deemed price of $0.25 per share ($2.5 million) and a cash payment of $125,000.

In late 2016, a Green Tree dispensary in Ottawa got busted, there was an unseemly fallout, covered in expert detail by Vice magazine.

When we finally managed to track down alleged Green Tree boss Robert Clarke, who is currently facing trafficking charges in BC,” wrote Vice, “he flew into a tirade over the phone, referring to this reporter as a “bitch” and a “fucking cunt.”

At that time, Green Tree was reportedly run by May Joan Liu – who was previously entangled in a penny stock scandal, and – in a separate incident – was charged with possession of cannabis for the purpose of trafficking.

In the Vice article, Ms. Liu “claimed she has nothing to do with Green Tree but conceded that her son, Justin Liu, may have some involvement.”

When Justin Liu was contacted by phone, he asked, “Are a reporter?” The Vice journalist replied, “Yes”. Mr. Liu hung up.

Vice described the Green Tree ownership structure as “deliberately opaque”.

Now follow the bouncing ball.

Because Winston Resources, and Justin Liu – are key actors in the Abattis story, which also features “deliberately opaque” structures and transactions.

On December 14, 2017 – ATT announced a financing, with included 7,222,222 shares purchased by Justin Liu at 18 cents.

On public documents, Mr. Liu’s address is listed as 1066 Groveland Road, West Vancouver. It’s a 1-acre property, owned by his mother, with a 7,000 square foot home, including a swimming pool and tennis court – assessed value: $6.2 million.

On January 12, 2018 Abattis acquired all the issued and outstanding common shares of Green Tree for $14.4 million in an all stock deal.

At the same time as the Cannanumus deal was being triggered, that and the value of Green Tree appears to have appreciated 570% in 60 days. In this transaction – Justin Liu received 10,950,000 shares of ATT. Abenante signed off on the deal.

The Form 9 document stated that the negotiation was “arms length” – which Investopedia defines as one in which the buyers and sellers of a product act independently and do not have any relationship to each other.

A January 19, 2018 Form 9 document, stated that the calculation valuation, dated January 8, 2017, determined an implied value of $24.6 million for Green Tree, using the “discounted cash flow method”.

This calculation valuation was prepared by Simran Gill Consulting.

Simran Gill (CFA) is also a partner at Bridgemark Financial. According to 4-Traders, Gill’s “personal network” is headed by Anthony Jackson.

Without formal legal training, we can not determine whether the acquisition of Green Tree by Abattis meets the legal definition of “arms length.” A cursory journalistic sniff reveals a pungent odor.

If you think that deal smells rank – check out Cannanumus.

Cannanumus was “developing a crypto currency which will link investors with cannabis producing companies,” but didn’t (and doesn’t) appear to have a website. The domain www.cannanumus.com was registered on 2017-10-25 and is ‘parked’ at SureSupport LLC Hosting.

We can find no evidence of employees, customers or revenues but never-the-less Abenante announced that he was “excited” about the Cannanumus deal.

And Cannanumus was founded by – wait for it – Simran Gill.

“We looked at many companies to partner with and Abattis came out on top”, stated Gill, “Through their growing portfolio of downstream products and services, Abattis can offer synergistic value to the coin.”

For the record – the Equity Guru brain-trust can also “offer synergistic value to the coin”.

So can the office cleaning lady.

And our pet gold fish (who just died).

Two days later, on February 10, 2018 Mr. Jackson was replaced as Abattis’ CFO.

Apparently, having supervised the $7 million purchase of a zombie company from a Bridgemark associate in his “personal network,” Mr. Jackson’s work at Abattis was done.

On February 26, 2018, Abattis release its Consolidated Interim Financial Statement for the 3-month period ending December 31, 2017. The company booked “other income” of $8,495 against “Management and Consulting Fees” of $5,132,640.

Was the CEO, Rob Abenante asleep at the wheel? If so, when he woke up, he was significantly wealthier.

He wasn’t poor when he fell asleep, truth be told.

During the nine months ended June 30, 2018, the Company issued 14,177,625 common shares to the CEO for the achievement of milestones.

“Milestones..” Adorable.

On February 27, 2018 Abenante received ATT shares worth $1.7 million. 12 days later he received additional ATT shares worth $810,000.

On May 24, 2018 Winston Resources announced that it will distribute 15 million common shares of Abattis to Winston shareholders.

According to the press release, Winston’s Board of Directors believes that distribution will “provide Winston Shareholders with investment flexibility, as they will hold a direct interest in two companies each of which is focused on different objectives.”

The deal was signed. The hold on the ATT shares expired 24 hours later.

Rob Abenante may be spread too thin. He is defending himself against a lawsuit from Blox Inc (BLXX.OTC) in the Supreme Court of BC.

The suit claims that – when Abenante was president of Blox – he made unauthorised payments to himself and his affiliated companies. These accusations have not been proven in a court of law.

Currently, as well as running Abattis, Abenante is also the CEO of Marifil Mines (MFM.V) – a lithium, gold and cobalt explorer in Argentina.

On August 28, 2018 ATT announced plans to launch a new line of pain relief products.

“We are very proud to have developed two products that safely reduce pain and modulate inflammation.” stated Dr. Brazos Minshew, President of the ATT Medical Advisory Board. A registered “Health Coach”, Dr. Minshew believes that, “Every person is creative, resourceful and whole.”

In 2017, Dr. Minshew appeared on a fake news radio show that was shut down by the Federal Trade Commission (FTC) after is was determined that “Dr. Minshew is not actually an expert in neurology or brain science, as claimed in the radio ad.”

Unfortunately, the story of ATT and its carousel of pantomime villains – is not a one-off.

A 2015 Financial Post article, Inside Canada’s Expanding Universe of ‘Shell’ Companies stated that, “Winston Resources is the root company in a network that has spawned more than 50 spin-off firms.”

Sounds like a slam dunk, doesn’t it? Like maybe someone, somewhere, who might police the public markets should be able to run these arseholes out of town on a rail?

The Investment Industry Regulatory Organization of Canada (IIROC), “writes the rules” and “investigates misconduct” on the public markets. During the last 10 years IIROC has amassed $32 million in uncollected fines. IIROC is currently funded by the same companies it is regulating.

Self-serving financially-educated young men can not be faulted for enriching themselves in this largely un-policed ecosystem. Like the Spotted Hyena, Bridgemark Financial, Anthony Jackson (CPA), Justin Liu (WTF) and Rob Abenante are following the rules of nature, gleefully ripping off the flesh of retail investors who come to the watering hole without first checking for bloodstains.

UPDATE: Shortly after we filed this story, Abattis announced they had completed their September 2018 year end financial audit. One down, Q1 and Q2 to go.

UPDATE II: Company says it is not delisting after all, as per the year ends being filed, but will remain suspended.

— Chris Parry and Lukas Kane

FULL DISCLOSURE: You can bet we have nothing to do with this mob in any commercial way, shape or form.

Leave a Reply