The recent rise in oil prices might be to blame for the failure of stock markets to extend their momentum. Oil prices are rising as Summer nears an end and investors are worried that higher prices will translate to an uptick in inflation data. This means hawkish central banks… and the possibility that interest rates will need to head higher.

With this rise in inflation, the next CPI data will definitely be worth watching. As energy rises, the cost for transportation increases. Businesses then pass off those costs to the consumers resulting in higher prices and thus resulting in an uptick in inflation.

A few days ago, many financial media websites were stating that this rise in oil could spook the markets. With the technicals indicating higher prices still to come, the markets are really going to be tested given the inflationary pressures this oil jump will bring.

In terms of fundamentals, this rise is due to the Saudi’s announcing they would extend their production cuts (1,000,000 bpd) until the end of the year and Russia announcing it would extend its export cuts of 300,000 barrels per day (bpd) for the same period. Both OPEC+ members claim this is to maintain the stability and balance in the oil markets. But many see this as a cash grab.

If you delve into the realm of geopolitics, this move is very interesting. The Biden Administration in the past have warned the Saudi’s of not towing the line. While the US is dumping emergency reserves to lower the price of oil to taper inflation, their Saudi allies have been taking opposite actions to increase the price of oil. In a way you cannot blame them since the Kingdom (the Royal Family) makes bank with higher oil prices. But the US is seeing this as the Saudi’s not acting as a proper ally… an ally which can count on US military support.

Many analysts have said the Saudis are turning to the East. For the first time ever this year, a Chinese diplomatic plane landed in Saudi Arabia and got the Sunni’s and Shia to shake hands. Saudi Arabia and Iran got back to recognizing each other and opening diplomatic channels. The Chinese in return ensured that they oil they get from the Middle East remains secure.

Last week, this idea of the Saudi’s flipping took an interesting turn. Both Saudi Arabia and Iran were included in the list of countries that will be joining the BRICS alliance (Brazil, Russia, India, China and South Africa) in 2024. Other nations joining include Argentina, Egypt, Ethiopia and the United Arab Emirates. Some see this as a major move which could result in the end of Dollar hegemony with the Saudi’s potentially announcing they will accept other currencies and not just Dollars for their oil. A bold and paradigm shifting move given the Saudi’s are the integral part of the petrodollar system. And perhaps they will feel bold to make this statement knowing they will have Russian and Chinese military support. The last part is just hypothetical. In reality, it is most likely that the Saudi’s and the UAE will play both sides.

All of this ensures the oil markets will be seeing some action in the next few months.

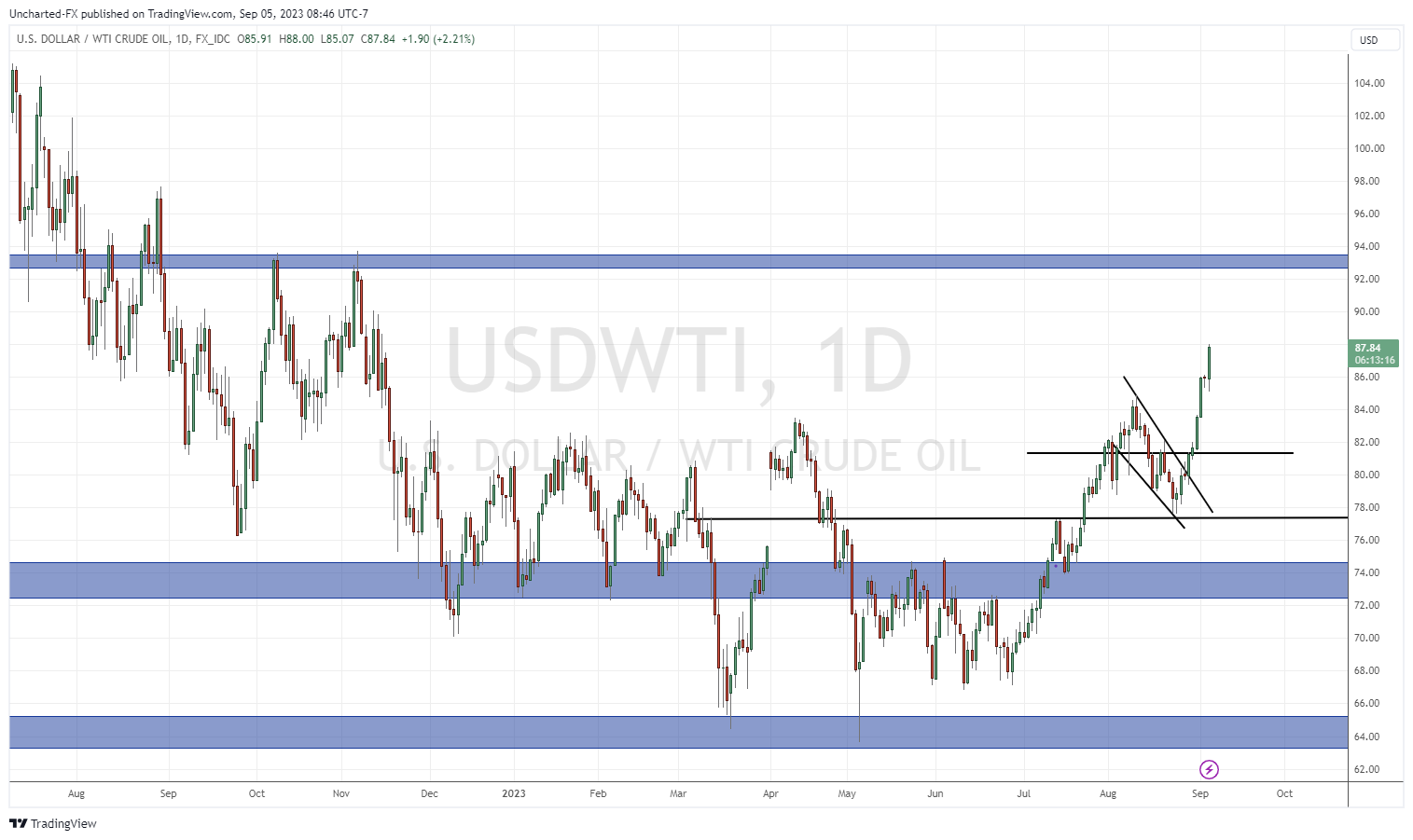

West Texas Oil is popping and has just passed $87 a barrel today. For those who follow my videos and Market Moment articles, I told followers that oil closing above the $75 zone was a major technical shift. In terms of market structure, the oil market ended its long range and a new uptrend was initiating.

Now, this uptrend remains intact with multiple higher low swings and even a correction being bought up on the test of support. With oil losing above recent highs at $84, the next resistance zone comes in around the $93 zone… and then $100.

Putting it simply: oil looks ready to go back above $90.

The chart of Brent Crude Oil looks exactly the same. Great technicals, and a breakout sets us up for a move to above $96.

How else can one play this oil move?

The Canadian Loonie is positively correlated with oil. When oil rises, so does the Canadian Loonie. This correlation isn’t 100% but is pretty high. Although currently, it appears that the US dollar strength is battering all other fiats including the Loonie. The CAD is at the important $1.3650 zone and could see buyers step in here. The large wick so far is encouraging.

The Canadian stock market is also predominantly composed of energy companies. If oil rises, so do these companies which moves the entire TSX. The set up is intriguing given the TSX recently closed above the previous lower high at 20,400. But as you can see from the chart, a major resistance zone is nearby. Prudent traders would wait for this to break before going long.

For ETF traders/investors, XLE is about to test a key resistance zone after a few days of gapping up due to the rise in energy. A breakout here would be bullish and set us up for a potential retest of previous record all time highs at $100.

And an added bonus. Natural Gas looks like it is ready to go. From a seasonality perspective, demand is about to rise as colder weather approaches. A lot of eyes will turn to Europe once again. Last year, many analysts believe Europe was saved by the warmest Winter ever recorded on the Continent. Will we see this again? Or will we finally see that energy crisis due to colder weather that many analysts have been warning of.

A breakout above $3.00 gets natural gas moving. And this market is very volatile. A breakout would see big follow through momentum on the way to $5.00. A close below $2.50 would nullify and upside breakout potential.

Leave a Reply