On August 30 this summer, we posted a story about a resource explorer called Lithium Ionic (LTH.V), in which we said:

Lithium Ionic isn’t out there asking investors to help them finance a drill hole in the hope they’ll find something.

They found something.

They’ve got something.

We then made the case for LTH being a deal that had already largely proven out what potential it had, and that from here on it was less a case of ‘if’ than ‘how.’

- On that day, you could have bought the stock for $0.68.

- The day after our story went out to our investor list, it would have cost you $0.75.

- Three months later, almost to the day, and it’ll cost $0.93.

I don’t know how much clearer we can make it to you, but the thing hasn’t stopped yet, and yet you’re still watching from the sidelines?

Giddy up, man.

Here’s what we were interested in back in August.

In May, 2024, a robust feasibility study demonstrated a 14-year mine life, average annual production of 178,000 tonnes of high-quality 5.5 per cent Li2O (lithium oxide) spodumene concentrate (24,200 tonnes per annum lithium carbonate equivalent), and competitive on-site operating costs of $444 (U.S.) per tonne.

But to get there, the company would need to spend USD $266,000,000, which is no small task.

This is where most junior resource explorers would start looking for a big partner to cover their bills, like a pole dancer trying to make her way through law school.

But the girls with the best GPA don’t need a sugar daddy, they just go straight to the bank.

Lithium Ionic Corp. has received a non-binding letter of interest (LOI) from the Export-Import Bank of the United States (EXIM) to provide up to $266-million (U.S.) in debt financing for its 100-per-cent-owned flagship Bandeira lithium project, located in Minas Gerais, Brazil. This financing represents 100 per cent of the capital expenditure (capex) outlined in the May, 2024, feasibility study, marking a pivotal milestone as the company accelerates toward construction and production within the next two years.

Translated for the layman: Lithium Ionic isn’t waiting about for a big investor to finance its next steps, rather it’s gone to the bank and said, “Give us USD $266,000,000, and the bank has said. “Works for us.”

That’s balls out, big boy trousers time.

And they’ve got 15 years to pay it back, which is longer than the life of the mine.

In essence, the bank has said ‘build it, start it, run it for 15 years and when you’re done, get back at us.’

Why would any bank be so agreeable?

A few reasons:

- This bank is the official export credit agency of the United States, which helps to finance projects that will help the US balance its import/export trade.

- This project will fit beautifully into the credit agencys ‘China and Transofrmational Export Program’ which seeks to help bring critical mineral production back under US control for the purposes of “energy security and electrification.”

- The project is grand.

How grand?

- High grade

- Large scale

- Low cost

- Hard rocks, not brines

- PEA and feasibility study completed

- Multiple NI 43-101s completed

- $20 million royalty deal banked

- Company raised money at a premium to market

- They’re still expanding the resource

- And acquiring new ground

- Mining friendly jurisdiction in a region with big wins already producing

- Right on the border of a company that just got bought up by a giant

In addition:

- The Feasibility Study indicates a post-tax Net Present Value (NPV) of US$1.3 billion and an Internal Rate of Return (IRR) of 40%, highlighting its strong economic potential.

- On an infrastructure level, being as it’s situated in Brazil’s ‘Lithium Valley,’ the project benefits from excellent infrastructure, including low-cost hydroelectric power, established transport networks, and proximity to international markets via nearby ports, enhancing its cost efficiency and competitiveness.

- Once due diligence is complete, with cash in hand the project should take just two years to finish.

This project is an arbitrage, people. At this stage of its life, most resource explorers have a high risk that they won’t be able to find financing to move to production, or that they’ll only raise a portion of it, or that the terms will be rough, or that someone bigger will be needed to give the project enough heft that banks will come in.

LITHIUM IONIC MISSED THAT MEMO.

They just jumped right into what’s next, as they have at EVERY STAGE OF THEIR DEVELOPMENT.

Yes, the fact that they’re building something the US government sees as a strategic imperative is obviously a large part of how they’ve managed to pull down all those digits.

That the US Southern Command and State Department felt comfortable adding their heft to the application tells you not only there’s a ready buyer for the end product, but also that the LTH manageent team have passed the military sniff check. If Southcom is prepared to sign your loan application, I’m not sure how much more a bank could ask for.

In fact, it appears LTH has graduated from explorer to this terminology, found on the front page of their website;

They’re not alone. There are already 300 producers in the region of the Bandeira deposit, so the area is not exactly a mystery from a geological perspective. The local regulators aren’t afraid of pulling thing out of the ground, there’s plentiful infrastructure to get lithium where it needs to be, and nobody needs to move mountains to get at it.

In short, this is a beauty, guys.

And, not to get all Ginsu Knives on you or anything, but ‘wait, there’s more.’

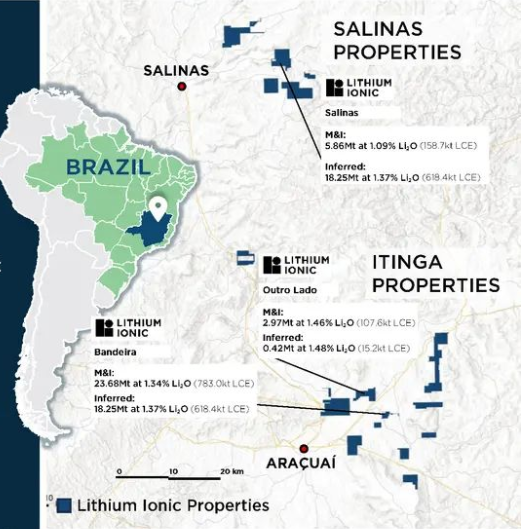

The Bandeira, which is the project we’ve been referring to so far, isn’t the whole kit and kaboodle. The company ALSO has the Outrol Lado claims, and the Salinas claims, which in and of themselves have plent of meat on the bones.

But the Bandeira, that’s the cherry right now.

BUT THERE’S MORE:

No, really.

On August 24, an announcement came that Pilbara was paying CAD $509,000,000 to take out Latin Resources (LRS.ASX), a nearby neaighbour with a claim at the Salinas properties.

RIGHT NOW, the market cap on LTH is just CAD $149,000,000, which means they’ve managed to get their hands on almost double their market cap in credit (assuming due diligence completes) while still having a standalone project that comparable neighbours received a more than 3x buyout for.

BOTTOM LINE:

- I can only drag you so far in this process, now it’s up to you.

- You have to be the one who sees the nuts and bolts here and decides it’s right for you.

- You have to be the one who talks to your financial advisor, or your partner, or your god, and decides whether this is right for you.

- I’m not going to tell you it’s a sure thing, though the temptation runs hard through me.

- I’m not going to make you promises on where this will end up, as due diuligence is a real thing, and the market gods have been known to throw curves and strikes.

But I’ll say this: These guys did what 95% of mining explorers never do. They got this to the line without slinging their asses around a pole.

I’m glad we spotted it.

Glad we bought some.

Glad we held it.

LTH?

LFG.

— Chris Parry

FULL DISCLOSURE: Not a client company. No commercial interest.

Leave a Reply