The offices of Emerita Resources (EMO.V) are abuzz right now, in that a decade long legal process to defend its perceived right to exploit the Aznalcóllar mine is finally coming to a head.

- If EMO wins the lawsuit, as is expected by many, the company will have the right to reopen a mine of significance in a region known for mines of significance.

- If it doesn’t win the lawsuit, that’ll suck, but it will still have significant properties that justify its present market cap.

- In short, the next few weeks bring the potential for a lot of upside.

Here’s how it is going down;

The Aznalcóllar mining court case in Spain centers on allegations of corruption during the awarding of the public tender for the Aznalcóllar mine redevelopment. This mine, located near Seville, was previously operational until a tailings dam failure in 1998 led to its closure. In 2015, the Spanish government initiated a tender process to reopen the mine, attracting bids from various companies, including Emerita Resources and a consortium comprising Minorbis and Grupo México.

Emerita Resources contended that the tender process was marred by irregularities and potential corruption, particularly favoring the Minorbis-Grupo México consortium despite their bid allegedly not meeting all required criteria. Emerita alleged representatives of the consortium had bragged to them that they had it locked in, and suggested EMO should work with the syndicate if it didn’t want to be left behind.

This led to legal challenges aiming to address these concerns and ensure a fair tendering process that, over the past several years, have been shown to have enough merit to bring charges.

As of March 3, 2025, the Third Section of the Provincial Court of Seville commenced hearings for the criminal trial addressing these alleged irregularities. The trial is expected to conclude by July 15, 2025, with up to 40 sessions scheduled during this period. Sixteen defendants, including members of the evaluation panel and individuals associated with Minorbis S.L., face charges such as influence peddling, fraud, embezzlement, and bribery related to the tender process.

David Gower, CEO of Emerita Resources, has emphasized that this phase represents the culmination of a decade-long process. According to Emerita’s legal counsel, under Spanish law, if a crime is committed in awarding a public tender, the offending bid must be disqualified, and the tender awarded to the next qualified bidder. In this case, Emerita asserts that it is the sole qualified bidder.

The outcome of this trial holds significant implications for the future development of the Aznalcóllar mine and the enforcement of transparent practices in public tender processes within Spain, but the consequences for Emerita Mining could be gigantic.

But before we dig on on the Aznalcóllar, let’s look at what else Emerita owns:

Iberian Belt West (IBW) Project

For the technical nerds:

The IBW Project spans approximately 12 kilometers and is accessible via paved and all-weather gravel roads. In March 2025, Emerita announced an updated NI 43-101 compliant mineral resource estimate for the IBW Project, reporting a combined 18.96 million tonnes (Mt) in the Indicated category at 8.44% ZnEq and 6.80 Mt in the Inferred category at 8.72% ZnEq. This update reflects a 35% increase in Total Indicated Mineral Resource tonnage and a 44% increase in Total Inferred Mineral Resource tonnage compared to the 2023 estimate. The project hosts three primary deposits: La Romanera, La Infanta, and El Cura, all of which remain open for further exploration and expansion.

For the retail crowd:

The IBW is a large mineral exploration area about 12 km long, in one of the most famous mining regions in Europe – the Iberian Pyrite Belt. This area is known for producing metals like zinc, copper, lead, silver, and gold.

What they’ve found:

There are three main zones of mineralization at IBW:

-

La Romanera – the largest and most promising, where most of the drilling has been focused.

-

La Infanta – a high-grade zone that was partially mined decades ago.

-

El Cura – a newer discovery with encouraging early drill results.

As of early 2025, Emerita has identified:

-

19 million tonnes of rock with valuable metal content in the “Indicated” category (which means fairly well-defined).

-

Another 7 million tonnes in the “Inferred” category (less certain, but still promising).

What it means:

The metals in these rocks are valuable, especially zinc and copper, which are used in everything from construction to electronics. These findings suggest the IBW Project could become a significant mine in the future, especially since the mineralized zones are still open – meaning more drilling could lead to even bigger discoveries.

What others say:

According to a December 30 report by Varun Arora of Clarus Securities, Emerita Resources Corp.’s recent metallurgical advancements significantly improved the economic potential of IBW. Clarus updated its model to reflect the latest results, noting that enhanced metal recoveries made the project’s economics more compelling. Arora stated, “Overall, we think this is an impactful update that further strengthens our view of the potential for compelling economics at IBW.”

The bottom line:

Let’s assume Emerita gets nothing out of the courtroom. Worst case scenario, the case crumbles and EMO is forced to make do with the IBW.

The upside on that is still epic, and the company has been actively progressing the IBW in the ASSUMPTION that it will be their primary project going forward. In my opinion, the valuation of the company as things stand is justified based on the IBW alone.

But they have more!

The Nuevo Tintillo Project

Located in Seville Province, the Nuevo Tintillo Project covers an area of 6,875 hectares along an east-west axis of approximately 25 kilometers. Situated between the world-class deposits of Aznalcóllar to the southeast and Rio Tinto to the northwest, the area has a rich history of mining dating back to the 19th century. In 2024, Emerita conducted greenfield exploration, including surface sampling that identified gold-bearing rocks exposed at the surface, with grab samples returning up to 2.04 g/t Au and 165 g/t Ag. Additionally, a pilot drill hole intercepted mineralized horizons, indicating potential for further exploration.

What Emerita is doing there:

This is a greenfield project, which means it’s an early-stage exploration – they started from scratch, looking for new discoveries, and they haven’t been let down so far.

They’ve done:

-

Surface sampling – collecting rocks at the surface to test for metal content.

-

Drilling – early drilling has shown signs of mineralization (metals in the rock), which is a good first step.

What they’ve found:

-

Rock samples with gold (up to 2 grams per tonne) and silver (up to 165 grams per tonne).

-

Evidence of other metals as well, possibly including copper and lead.

Why it matters:

The fact that Emerita is finding precious metals at surface level, in an area with a strong mining history, suggests this could be a valuable new discovery. It’s still early days, but the signs are promising – and the location is ideal, surrounded by proven mines.

But wait, there’s more still!

The Ontario Property

Adjacent to the IBW Project, Emerita has been granted the Ontario exploration permit, which hosts several historic producing mines. Reconnaissance and preliminary evaluations have included sampling at historic waste dumps, with results confirming significant copper mineralization. For instance, samples from the San Jose mine area assayed up to 13.2% Cu, indicating the potential for additional exploration within this license area.

This project is located right next to Emerita’s main project (IBW) in southern Spain — despite the name “Ontario,” it has nothing to do with Canada. The “Ontario Property” is actually a permit area near the town of Paymogo, where there were historic mines that used to produce copper.

What Emerita is doing:

-

They’ve been granted an exploration permit to check out this area more thoroughly.

-

So far, they’ve done some early testing on old mine waste piles (called “waste dumps”) to see if there’s still metal left behind.

What they’ve found:

-

Very high-grade copper in some samples — up to 13.2% copper, which is considered excellent.

-

These findings suggest the area may still have untapped mineral potential, and further drilling could confirm that.

Why it matters:

-

It’s a low-risk exploration: there’s already proof that mining happened here before, so Emerita’s just trying to see how much good material is still left.

-

It’s also right next to their big IBW Project, which makes it easier and more efficient to explore and develop together.

IN SUMMARY:

Emerita has three – count em – three seemingly significant projects, all within a stones throw of one another, all of which they’ve been progressing, giving them short, mid-, and long term prospects that in their totality would, in my humble opinion, warrant their current $366m market cap – IF THAT’S ALL THEY HAD.

But the Aznalcóllar is the big dawg.

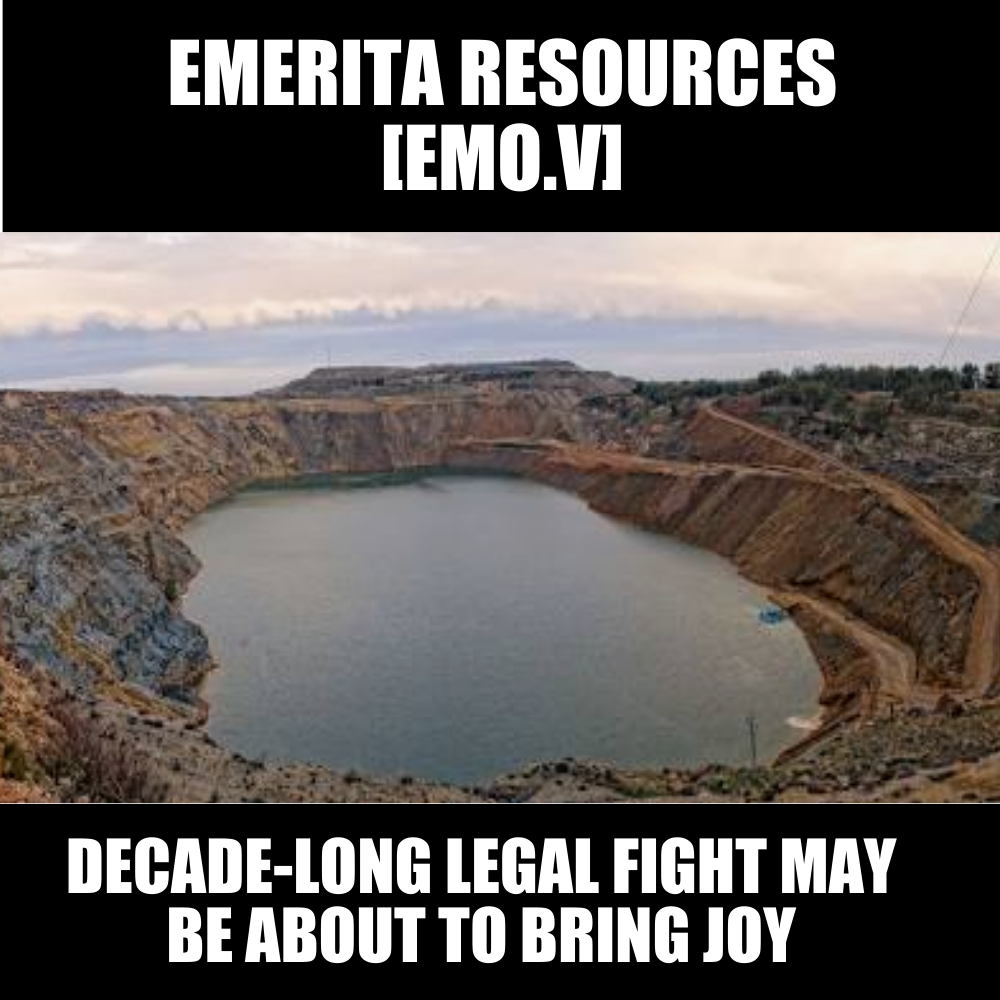

Where it is:

Aznalcóllar is a former mine in southern Spain, near Seville. It used to be one of the largest zinc and lead mines in Europe, but it was shut down in 1998 after a tailings dam failure. It’s been a political and legal football ever since.

-

If the court finds wrongdoing, Emerita could be awarded the rights to the mine. This would be a huge win — Aznalcóllar is considered a world-class asset, with potential for producing large amounts of zinc, lead, and silver.

As of 1990, combined reserves for the Aznalcóllar and Los Frailes operations were reported as follows:

-

Massive Pyrite Reserves: Approximately 43 million tonnes (Mt) with grades of 0.44% copper (Cu), 1.74% lead (Pb), 3.33% zinc (Zn), 67 grams per tonne (g/t) silver (Ag), and 1 g/t gold (Au).

-

Cupriferous Pyroclastics: An additional 47 Mt with grades of 0.58% Cu, 0.40% Zn, and 10 g/t Ag.

By January 1999, the Los Frailes deposit specifically had:

-

Proven and Probable Ore Reserves: 43 Mt at 0.3% Cu, 2.1% Pb, 3.7% Zn, and 58 g/t Ag.

-

Measured and Indicated Mineral Resources: An additional 30 Mt at similar grades.

Guys, that’s a bonafide beast.

Now I’ve been talking about this company, this mine, and this lawsuit for a few years now and the rallying cry has long been, “Some day that lawsuit will happen and this thing will get real very quickly.”

But as we all know, “some day” is an eternity in the public markets. Nobody wants to leave their capital locked up waiting for Spanish prosecutors to get a wriggle on with their case.

So while EMO has been on an upward trajectory for a while, that trajectory has been slow.

But now it’s happening.

My stance:

- All four projects have merit

- The three projects EMO owns currently justify the share price

- Lots of eyes are landing on EMO right now as the trials begin

- Multi-metal exposure in gold, silver, copper, lead, and zinc, among others

- The upside, upon a positive legal outcome, will be a monster

Do your own due diligence, but add this company to your watchlist either way.

— Chris Parry

FULL DISCLOSURE: Not a client, no commercial dog in the fight, but likely to buy stock in the days ahead

Leave a Reply